Housing Affordability

| Data Notes | |

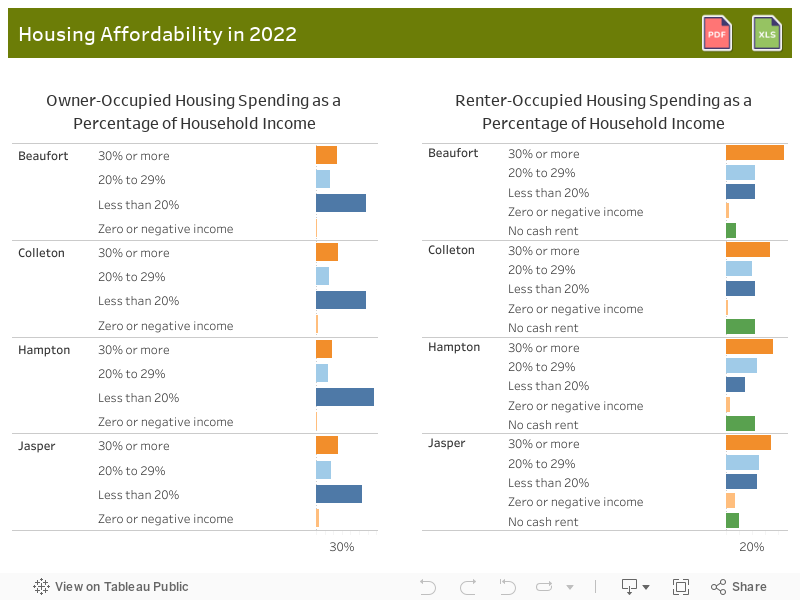

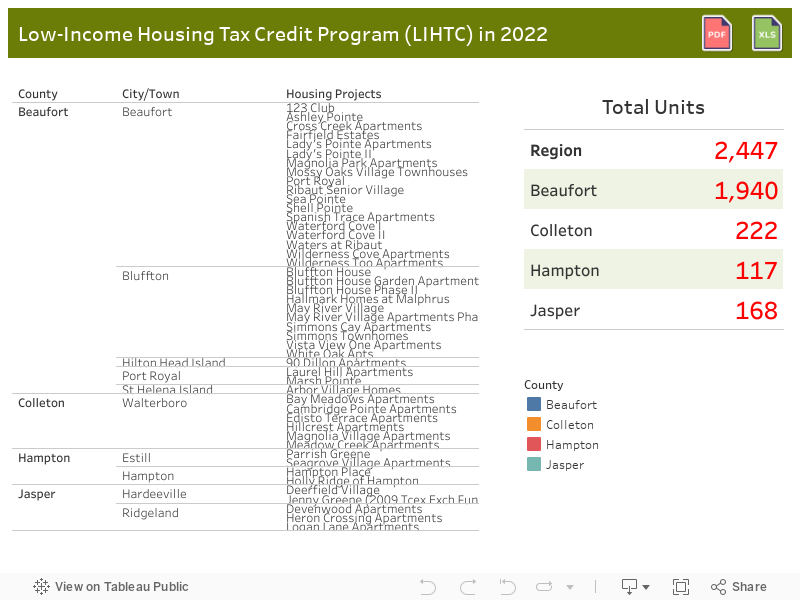

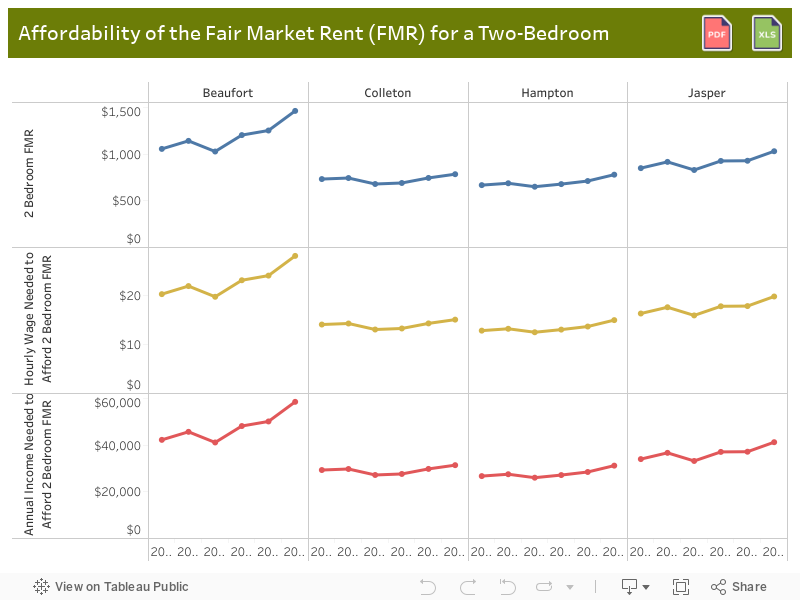

| Definition | Affordable Housing: Housing for which the occupant is paying no more than 30 percent of gross income for housing costs, including utilities. Low-Income Housing Tax Credit (LIHTC): Created by the Tax Reform Act of 1986, the LIHTC provides a tax incentive to construct or rehabilitate affordable rental housing for low-income households by subsidizing the acquisition, construction, and rehabilitation of affordable rental housing for low- and moderate-income tenants. Fair Market Rent (FMR): The FMR is developed by the U.S. Department of Housing and Urban Development (HUD) to determine payments for housing assistance programs like the Section 8 housing choice voucher program. No Cash Rent: The unit may be owned by friends or relatives who live elsewhere and who allow occupancy without charge. Rent-free houses or apartments may be provided to compensate caretakers, ministers, tenant farmers, sharecroppers, or others. |

| Data Source | U.S. Census Bureau, American Community Survey 5-Year Estimates; U.S. Department of Housing and Urban Development (HUD), Low-Income Housing Tax Credit Database; and National Low Income Housing Coalition, Out of Reach |

| Last Updated | April 2024 |